The Indexed Annuity Guide below contains more detail.

Learn How You Could Protect Your Retirement Accounts From Loss, Create Above Average Growth, & Create a Lifetime Income You Can Depend On.

Why Annuities

Planning for retirement can feel overwhelming. With taxes, inflation, healthcare costs, and stock market ups and downs, many seniors worry about running out of money.

Annuities are designed to combine safety, growth, and guaranteed income—all in one product. This guide will explain how annuities work, their benefits, and why they have become a foundation for retirement planning for millions of Americans.

Here are some specific areas we're going to cover.

Why Annuities Are A Smart Safe Choice.

Types of Annuities.

What can affect your choices such as Surrender Fees & Bonuses.

Timing & Planning in Annuities for your income needs.

How Indexed Annuities actually work to grow your money.

What affects growth in an indexed annuity behind the scenes.

Why Index Allocations are critical to growth.

Please do not feel like you have to commit all this to memory. This is just to give you an overview and initial understanding on what will help you, when you consider annuity options. You can always ask me any questions you have via phone, text, or email. I’ll help you get a clear understanding on everything.

What are the Biggest Concerns of Most Retirees?

Outliving your money – Will your savings last as long as you do? People are living longer than ever, and retirement may last 20–30 years.

Safety – Can you count on your money being there when you need it? Market downturns can quickly wipe out savings, which could take years to rebuild.

Taxes – Are you losing too much of your retirement income to the IRS? Many retirees donʼt realize their Social Security benefits can also be taxed.

Inflation–How will you keep up with rising costs of food, housing, and health care over time?

Indexed Annuity Benefits

Indexed annuities are built to address the above retirement worries and more.

They offer:

Principal protection—you will never lose money when the market goes down.

Growth potential—earn interest linked to stock market indexes, like the S&P 500, without risking your principal.

Tax deferral—earnings grow tax-deferred until you take them out, which may lower your current taxes.

Probate protection—your money goes directly to your loved ones, avoiding delays and expenses.

Flexibility—many contracts allow access to funds in emergencies, giving peace of mind.

Guaranteed lifetime income—turn your savings into a paycheck for life, with options to cover a spouse as well.

For these reasons, annuities have become a trusted option for those who want to enjoy retirement without constant financial worry.

Types of Annuities

There are 2 main types of Annuities - Fixed Rate and Indexed Annuities.

Fixed rate annuities have a fixed interest rate for growth, often low but guaranteed. It’s pretty basic.

Indexed annuities give you the option to get above average growth and provide a strong choice over lower fixed interest rate annuities.

Indexed annuities were designed to beat other safe fixed-based products like CD’s, Bonds, Straight Up Fixed Rate Annuities and MYGA’s.

The reason they are so popular is you can get market growth without the risk of loss when the market goes down.

You’ll see how these work in another section coming up. As we go forward, we’ll be focusing on indexed annuities, which are the most popular choice.

Considerations & Options in choosing an Indexed Annuity

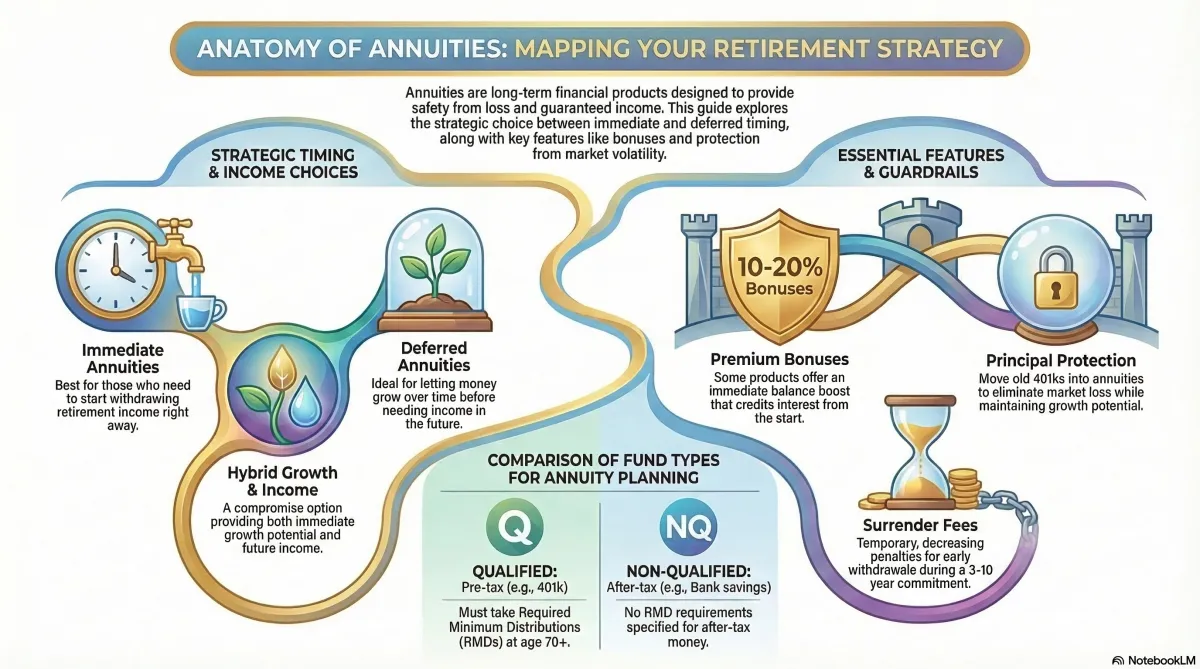

Considering Timing Choices - Immediate vs. Deferred Annuities.

This is about when you’lI want to use the money in your annuity.

You typically open an Immediate annuity if you need to start withdrawing income right away.

Otherwise you would choose a Deferred annuity to give your money time to grow, before you have the need for income in the future.

There are some products which are designed for both immediate growth and income. They can be a compromise on the gains you can reach with a standalone deferred or immediate annuity. But they are an excellent choice depending on specific circumstances.

Other components of an annuity.

These are important terms on annuities to understand.

Surrender fees

Annuities are long term financial products, usually for 3 to 10 years. When you choose a product to put your retirement savings into, the guarantees you receive, like safety from loss, comes from making a commitment in time.

If you cancel your agreement there are costs that have to be paid for. Surrender fees are like temporary penalties you incur in the beginning years of your long term commitment, in case you decide to pull all or too much money out at once, against the terms of our contract.

Expect surrender fees to start out high the first year and then go down each year until they reach zero.Bonuses

There are annuity products with bonuses, on your entire balance, when you open your annuity account. We typically see up to 10-20%. Imagine opening an annuity with $100,000 and after it’s opened you all of a sudden have $120,000 you’re earning interest on.

You get credited from the start, so you’re earning money on a higher balance immediately.

The bonus (as cash value) is released in your account over time, so no one can just open an account, get a bonus, and leave with the extra money. There are rules to this just like in everything else.

Besides using it as a boost for your account balance, a bonus can also be used to make up for a surrender fee being paid, when someone wants to move from an existing annuity, which may have been purchased during a very low interest rate period.Options

There are also optional riders in some products that offer features like Long Term Care. These have a cost and need to be looked at closely to see if it’s a real value to you or not.

Here are a few things to consider as you start looking at annuities.

These are questions which will help narrow down the annuity products which should best fit your needs.

What do you have in place for retirement income besides the money you’ll put into an annuity?

Have you looked at how much you’ll get from Social Security depending on when you start drawing on it?

You may want to use some annuity withdrawals to help you support your income in order to take social security later, when you’ll get a larger monthly check. The difference in the size of your monthly check can be substantial and would be for the rest of your life. If you don’t have a recent social security statement to help you see your options, create an account at ssa.govAre you looking for lifetime income, occasional withdrawals, money to leave behind for your family, or something else?

Is your money considered Qualified or Non Qualified?

Qualified money is where you put it into savings before paying taxes on it, like a 401k plan.Non Qualified is money you’ve already paid taxes on. Like cash you’ve saved in the bank or investments you made from after tax money.

Qualified money has rules to follow regarding access, taxes, and fees. Also, at a certain age (typically 70 or over). you have to start making Required Minimum Distributions (RMD’s) to start paying the taxes on that money.

If your money is currently in a Qualified account, you can typically move it into a qualified annuity and not have to pay taxes or fees when moving it over, unless you keep some of the money and don’t put it all into the annuity.

By the way, if you have an old 401k you aren’t contributing to anymore, which could be losing money every time the market goes down, you could move that into an annuity right away and never lose a dime again.

Plus you can still earn growth on it when the market is going up. It’s a great way to protect and grow that money you’ve already worked to save, rather than leaving it at risk.If you’re currently retired and need income now, you might look at an immediate annuity or a combination Growth & Income annuity.

Especially one with a bonus, depending on some other factors.If you’re not retired yet or have at least a few years to let your money grow, a deferred annuity is a more likely choice for you.

Depending on timing and how long you can let your money grow, a bonus could give you a 10-20% head start on growth, or you may have an opportunity for higher long term growth in a non-bonus product. These are details we go through when you’re ready to start looking at options.

There are other things to consider, like liquidity in case of emergency, which we talk about too when you’re ready to look at how an indexed annuity could work for you.

The Power of Indexed Annuities

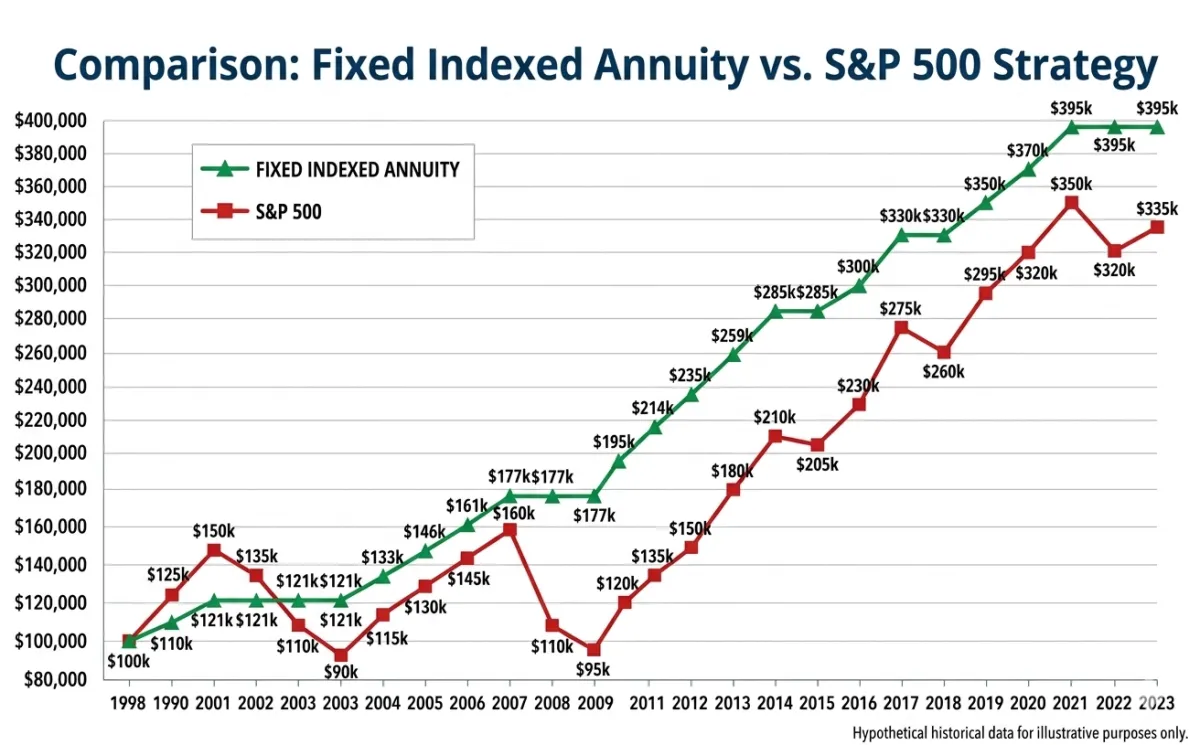

Below you will see an illustrated example of how an Indexed Annuity works to protect your savings while leveraging the market:

In the chart above, the Green Line represents an Indexed Annuity, and the Red Line represents traditional investments, such as a 401k, stocks, mutual funds, etc. In this case we use the S&P 500.

In nutshell, when the market is going up, the Indexed Annuity gains value. When the market goes down, the annuity stays where it is. When the market starts moving up again, the annuity moves up too.

An indexed annuity limits your loss to 0%, so if there is a market downturn, you never lose any of your principal.

When the market goes up, you can receive gains. This acts like a compounding affect.

With traditional investments, every time the market goes down, it can take a great deal of time for the market to come back and re-build the losses.

You don't have those losses in an annuity, so after a downturn, when the market is coming back up, it's building your account, not re-building and playing catch up.

Which line would you rather have your retirement follow?

This is one of the main reasons why indexed annuities are so popular.

How Indexed Annuities Work behind the scenes

Now we’re going to touch on an area most agents don’t understand and cannot easily explain to you.

Usually, they were just not taught about this.

This is how an indexed annuity works behind the scenes to keep your money safe and can create that above average growth for you over time.

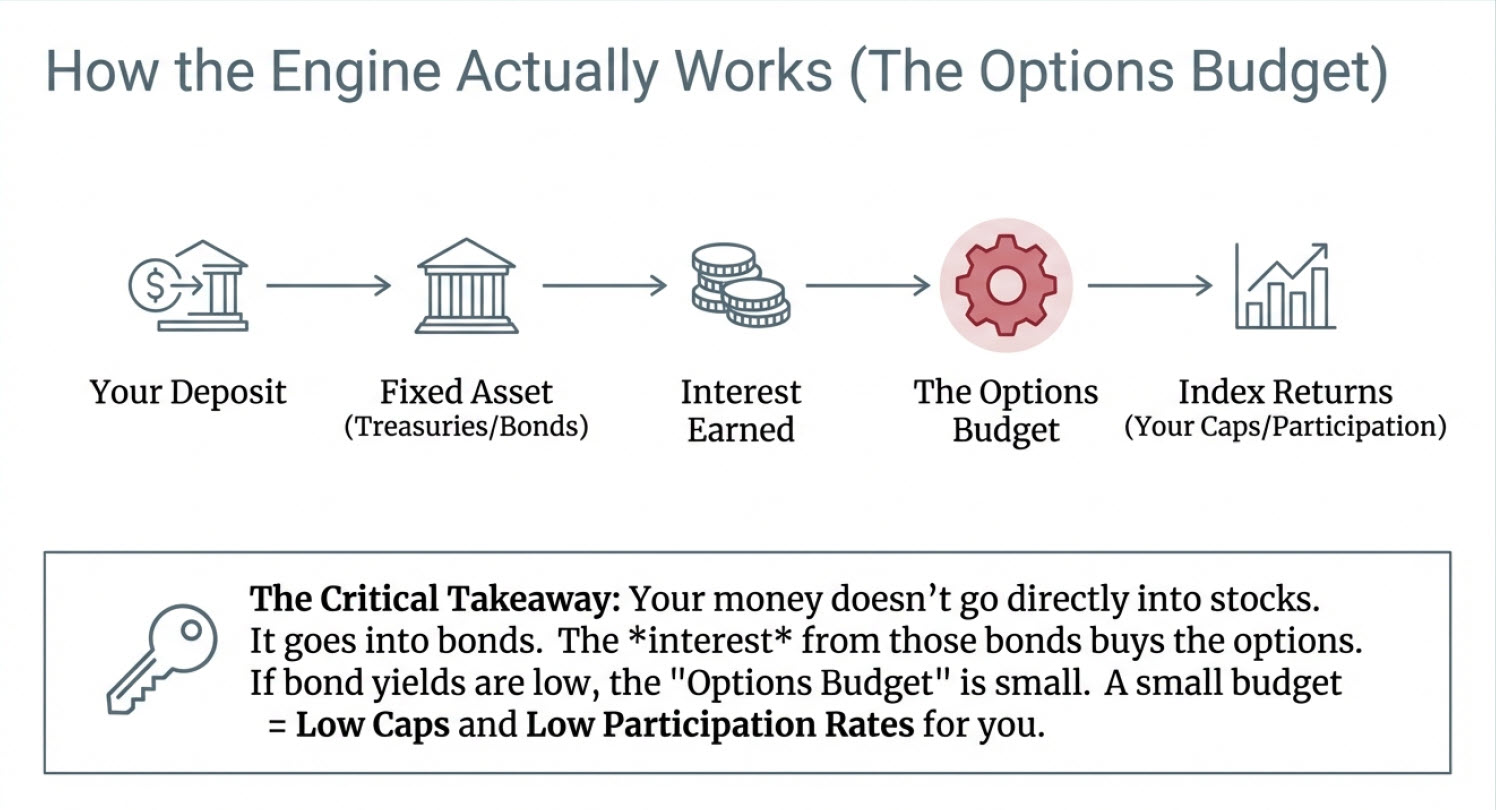

First, when you put your annuity in place, you deposit your money with the Insurance company.

The Insurance company places it into a fixed asset, usually a corporate bond or a treasury to protect your principle from any losses and have guaranteed interest to work with.

This guaranteed interest from the fixed asset, is what gets invested into what we’ll call an Options Budget.

The Options Budget pays for the options they purchase to drive growth in your account. An option is like a short term stock trade with limited risk. They buy options for the indexes you choose to allocate your money into (Index Allocations).

The profits from these options fuel your growth and pay for all the costs involved.

You’ll see how important your index allocations are in a minute.

Remember, while all this is going on, they are working with the options budget money.

Your account funds are safe inside the fixed asset!

What affects growth in an Indexed Annuity

These are factors that can affect growth, which is why you need to look at taking advantage of index allocations, which we talk about later.

Watching your annuity and updating your Index Allocations as needed will help you avoid missing out on additional growth.

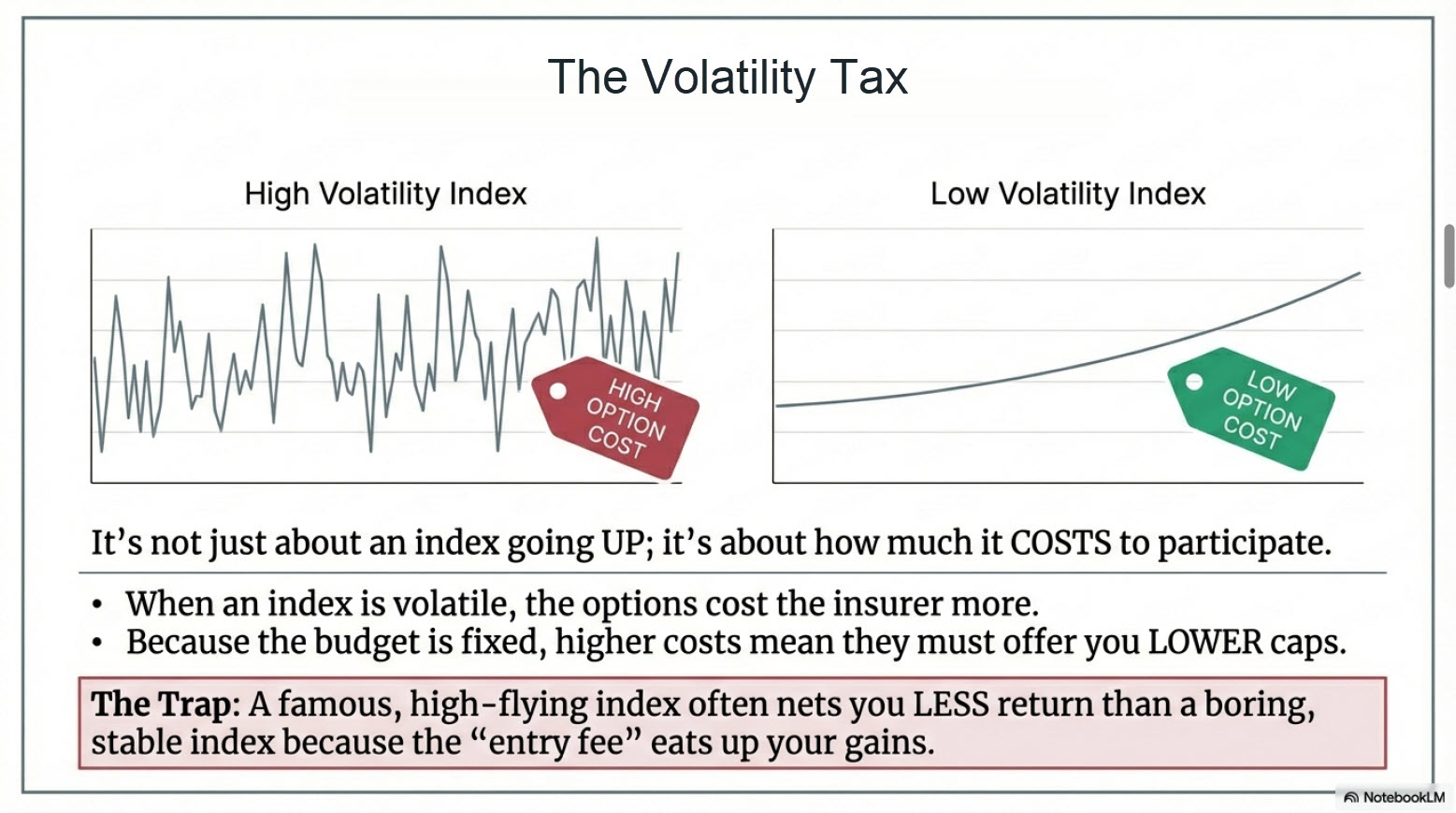

Volatility - Why Index Allocations are so important.

It’s easy to understand that when the market is going up, rising interest rates can generate growth.

While the rates are moving up and down, how far they move up and down from day to day or week to week is called volatility. You’ll see an example in the chart below.

When the volatility is very high, it causes the options being bought to become more expensive. But you still only have a fixed "options budget" to work with.

Each period end, you can choose to change your index allocations. For that year or period, the annuity company is obligated to pay you a specific share of the index growth, as stated in your contract.

You might have a certain Cap Rate, which is a limit on the interest rate improvement of the index rate growth. Or you may have a specific Participation Rate, which is a percentage of the growth.

Either way, if volatility raises the costs of the options, you may find that the next yearly period in your annuity contract is updated showing you’ll now receive a lower Cap or Participation Rate. This happens often when options costs have been rising due to volatilty.

This is why choosing your index allocations is critical and not something you can leave to chance. What appears to be an index with a high rate of return could have very little return, due to high volatility and high options costs.

With an analysis of your available index choices in your specific annuity, you'll know at each Index Allocation change period, what action to take if needed. And you won't be on your own. We create that analysis for you every year.

The Time Is Now.

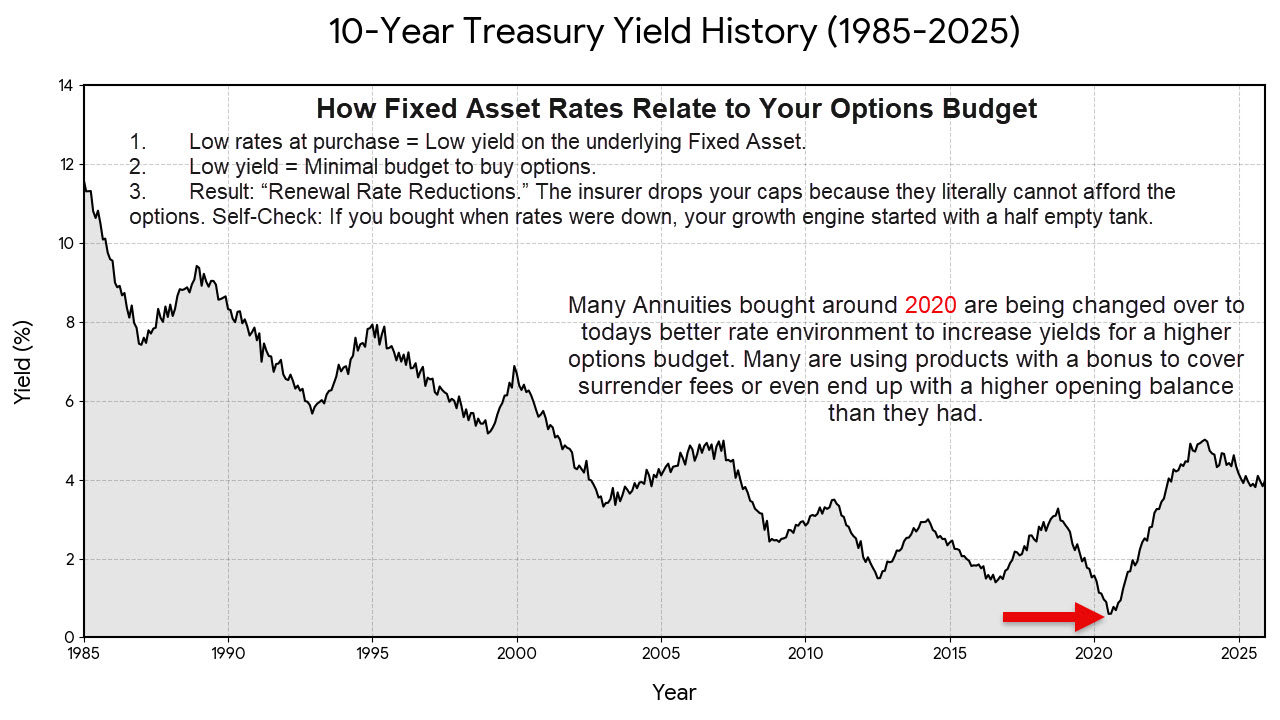

Another factor that affects growth is timing, or when you get your annuity.

Fortunately, this is a great time to start an annuity.

There were billions put into annuities back around 2020-2021 .

The rates on fixed returns were super low (effects from COVID).

Look at the Red Arrow on the chart above. That was not an ideal time to get into a fixed asset.

Think about how the options budget works. You are getting a fixed return in the options budget to pay for everything.

If the costs of buying options goes up and you have a fixed budget to buy them with, any increase in the costs of options means you can buy fewer of them, which means less opportunity for growth.

Many of those who bought annuities during that low rate era are now getting out of those products and getting annuities leveraging today's rates.

In many cases, people are getting annuities today with a bonus to pay for the surrender fee they have on the old annuity. Some even end up coming out ahead with bonus left over after paying the surrender fee.

You have access to annuity products today that were not available a few years ago. The opportunities today are excellent.

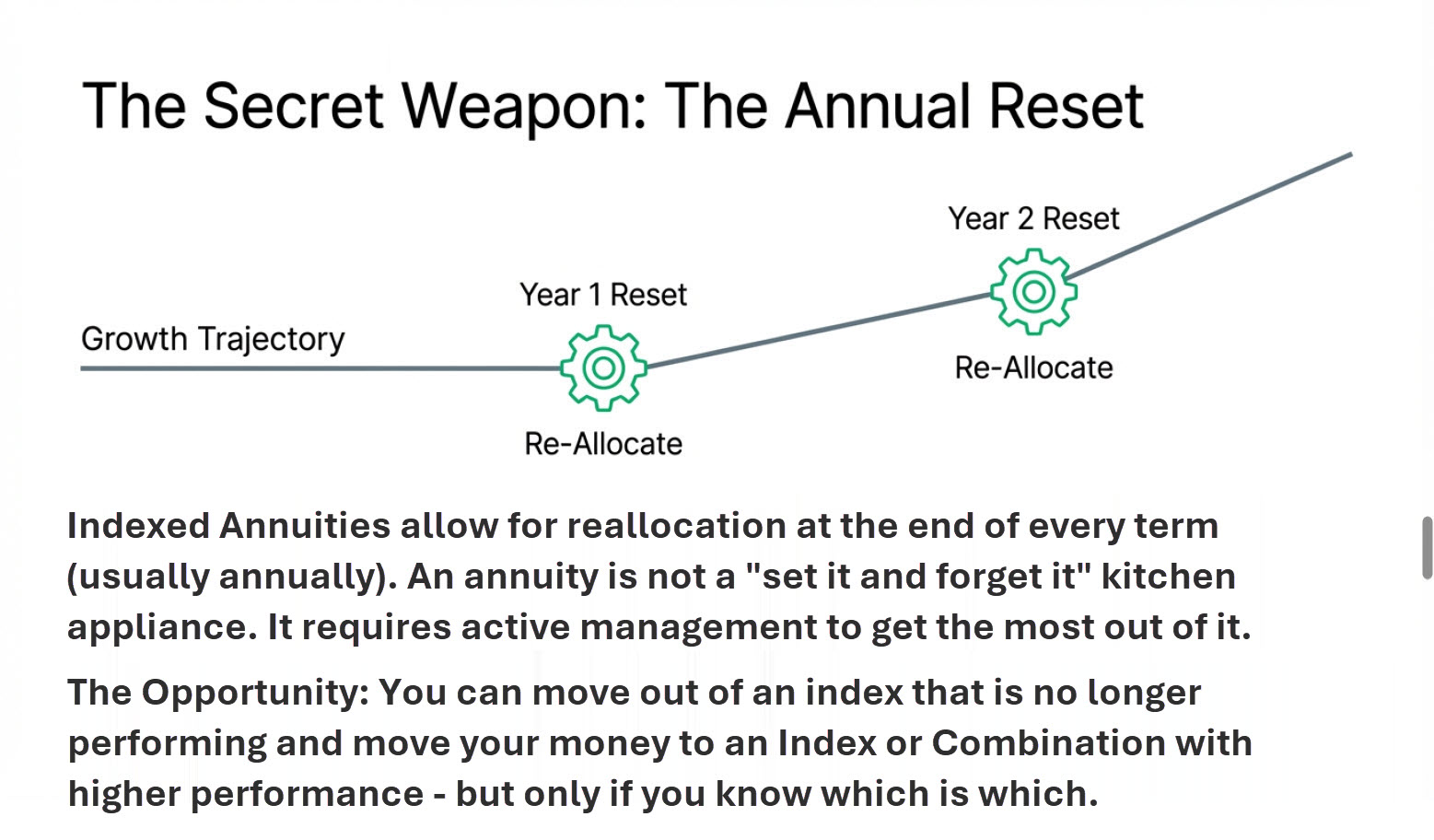

Index Allocations & Annual Resets

Unlike in a fixed rate annuity, where you don’t really have any choices to make after opening the account, you have a powerful tool in indexed annuities that can help you protect your growth.

You choose where and how much of your account to allocate to specific funds or indexes. These are called your Index Allocations.

You have the ability to reallocate your funds every period, typically a year at a time, called an Annual Reset. This allows you to make course corrections in case of unexpected index performance or other changes.

Now, you may choose to leave your allocations alone during an annual reset, or you may take advantage of a change to an allocation which now has a higher return.

Having these choices can help you build higher savings, as opposed to sitting in an index which started off great, then fell victim to high volatility and reduced returns.

When you hear the rare complaint about an indexed annuity not making as much as someone thought it should, you’ll typically find that they didn’t make any allocation changes on their yearly anniversary dates because they didn’t understand it.

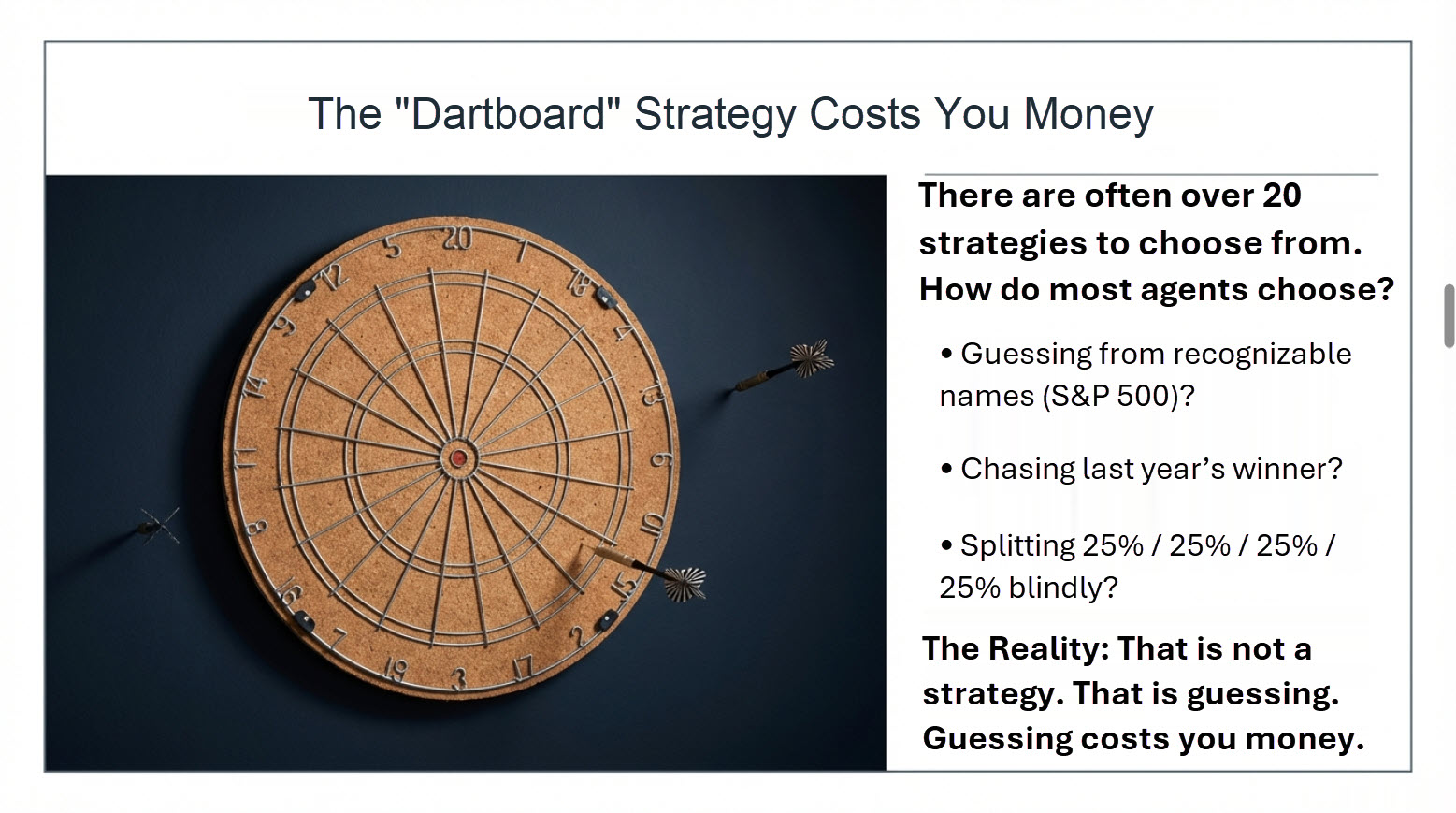

That is because most agents don't understand it well. So they can't explain it to their clients. And they don't have access to the systems that can create a yearly allocation analysis for you, which is based on real data.

Most agents just go by the carrier illustration, which is not designed to be a guide on choosing allocations. They don't contain enough data and make assumptions.

The agents often pick allocations based on the dartboard method you'll see below.

Basically, your agent is not using data to guide you, because they were not taught how to watch out for you after they get your annuity in place.

That's where their job usually ends.

With us, that's the beginning. We're here to help you get the most out of your annuity, from day 1 until you annuitize, or turn your annuity into a lifetime income.

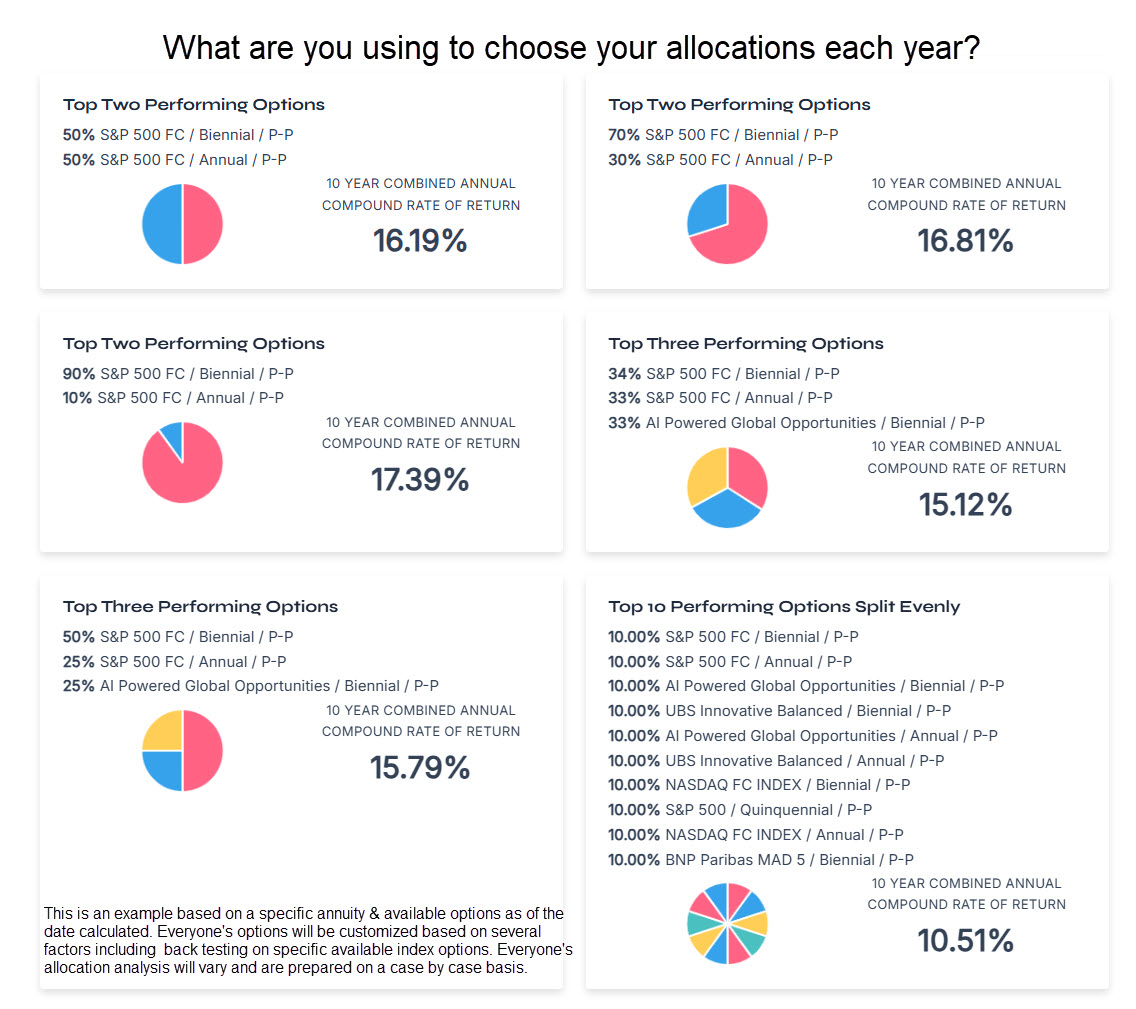

As you've seen, it’s important to look at your index allocations once a year, before your anniversary window is over. This is to compare your current index allocation to other options, to see if a change could benefit you over the next year.

Now, we're going to look at how make this easy for you. We start by creating an analysis to help you choose an annuity.

Then we create an updated analysis, based on all your available index options for you, every year. This is so you don’t get stuck in an underperforming index and lose out on higher growth.

You’ll see more on this next.

How should you make Index Allocation Choices?

Data beats throwing darts.

We take your financial security as serious as you do. By retirement age, there isn't any time to try to rebuild any losses in your savings. Time is critical now. Security and protection are key.

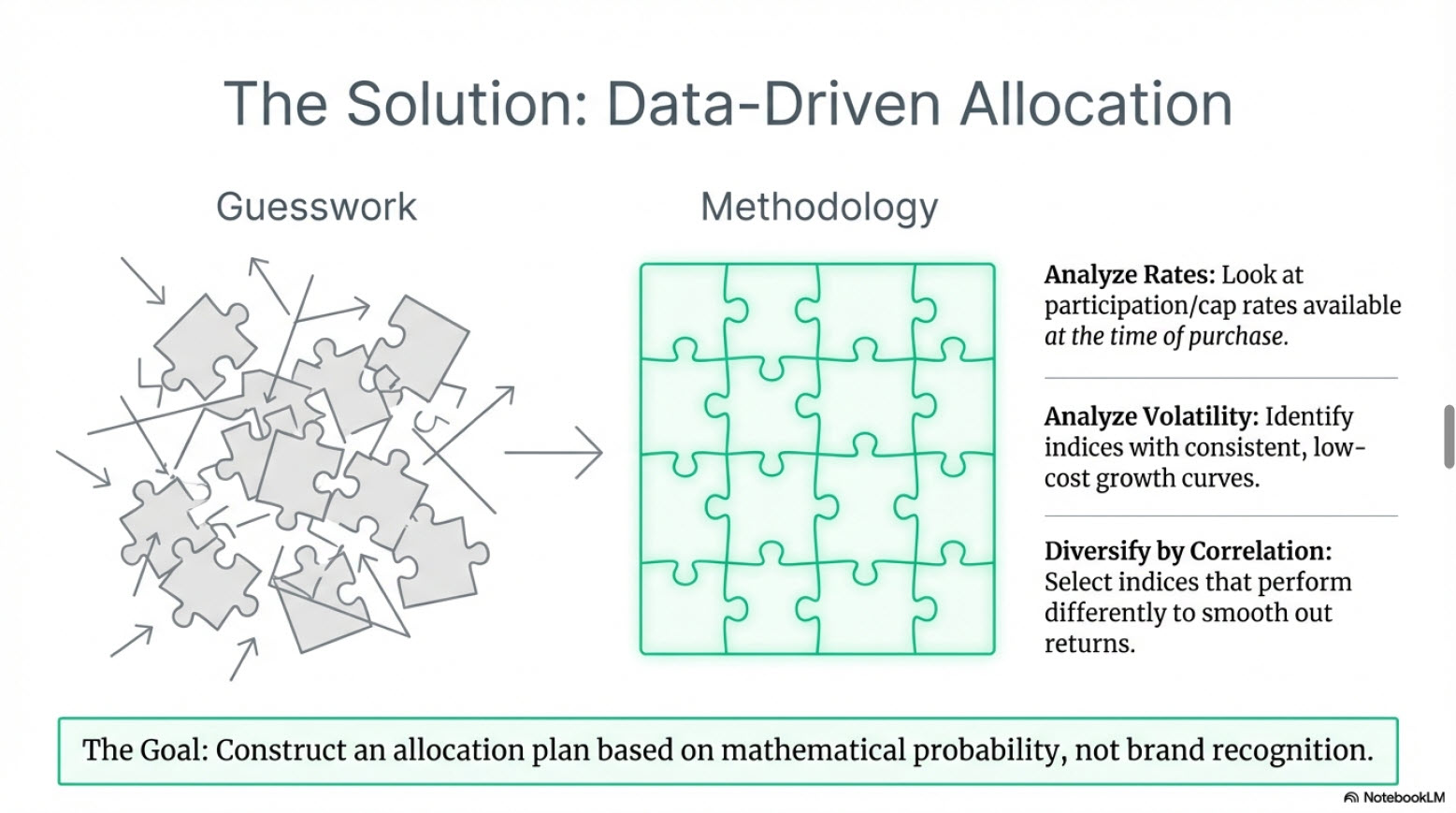

There is a lot of work to be done to find the most appropriate annuity product for you. After we talk to learn about your specific needs and situation, we start tp narrow down the annuity products that best fit.

Once we do that, then we start analyzing current data along with historical data to see which products you are interested in have the best returns.

Then we prepare an analysis to go over with you, to help you find the best product for you.

This is specific to your age, state you live in, and other factors that are important to you.

We're using current, up to date data. We also include items like the bonus available, if any.

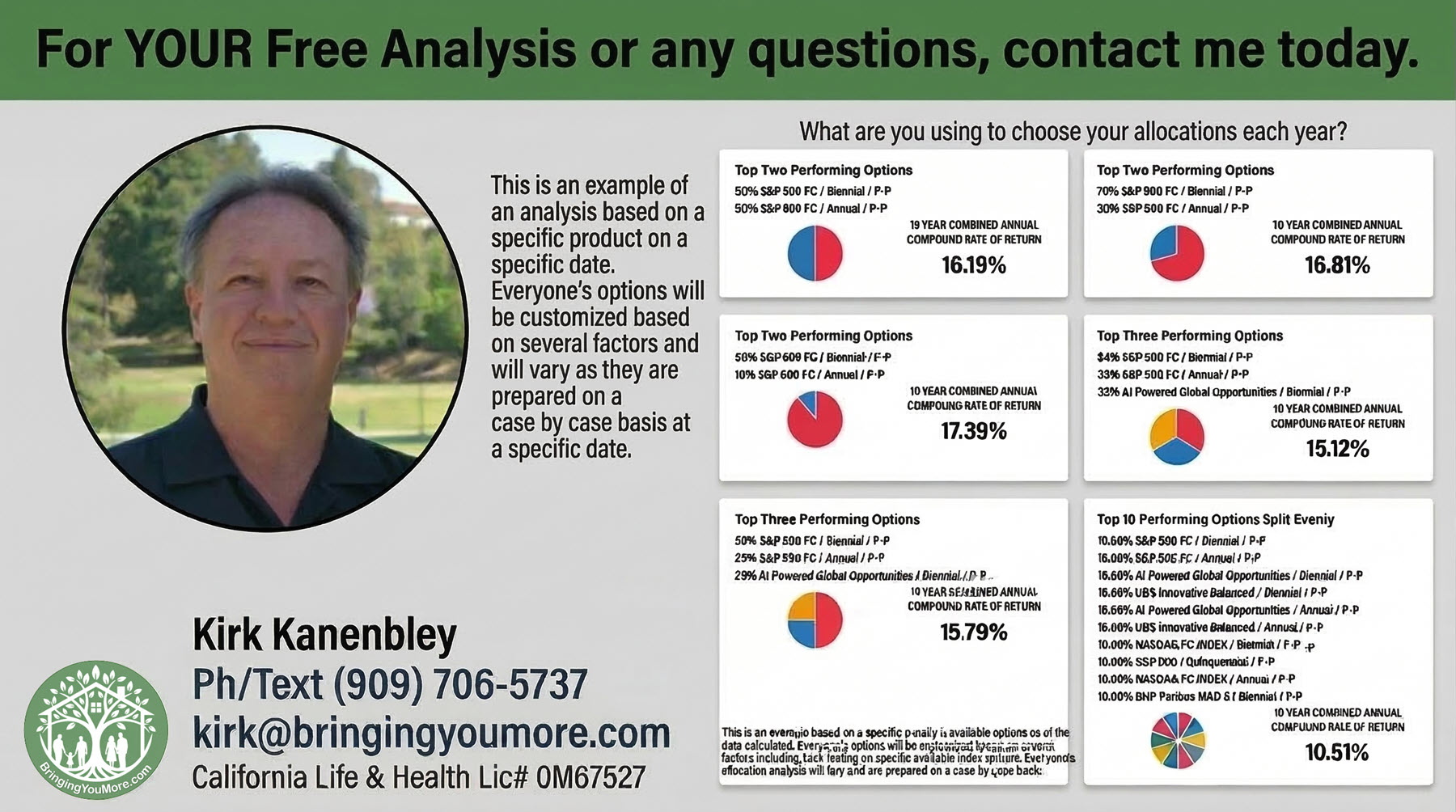

This is to find the annuity best suited for you. We want you to start off by choosing from the best performers. (see the image below)

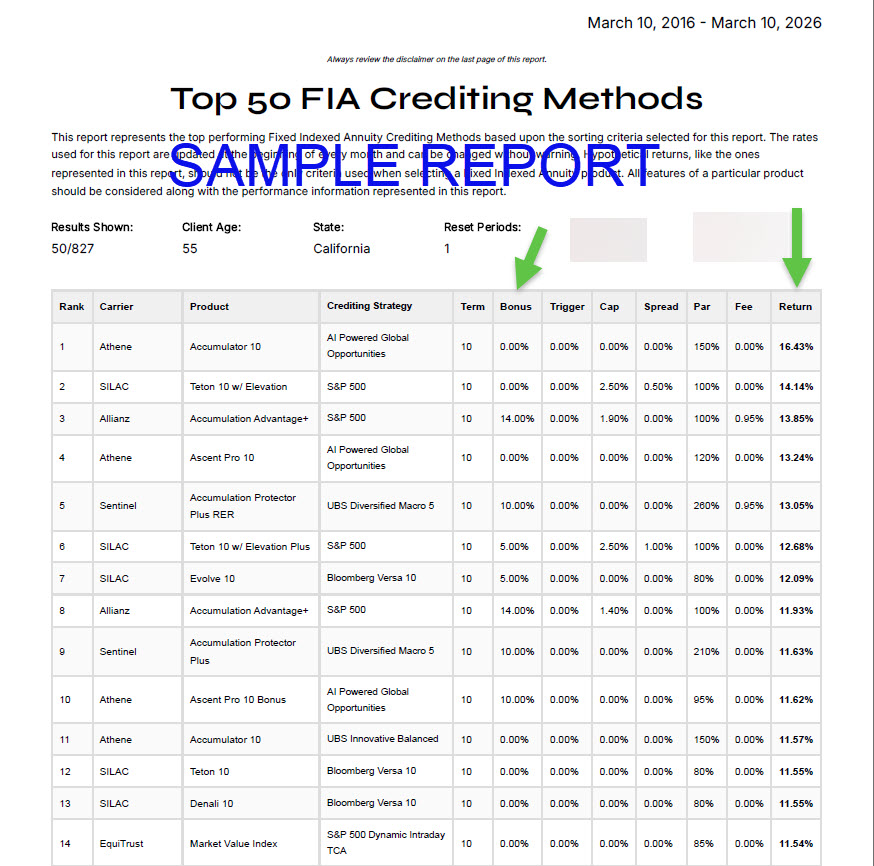

As you near your first annual reset, we'll prepare an analysis using all of the index allocation options available in your specific annuity.

Here's a sample from an analysis like you'll have, making it easy to see if a change is needed.

(see the image below)

You won't be on your own on this. We'll talk about the choices each year, before you update your allocations.

Remember, there are two things that will help you get the most growth out of your annuity. Taking a little time each year to see where you are and having the data to make the best decisions you can.

Final Thoughts

Indexed annuities are simple, safe, and designed for seniors or any individual who wants peace of mind.

They protect your savings, grow your money, reduce taxes, and can give you income for life.

With a long history of providing security and oversight from state-regulated insurance companies, they remain one of the most trusted retirement tools available today.

We Are Here to Help You

We help educate individuals on all the different retirement options, and we can help guide you through the process of maximizing your retirement to its fullest.

Contact Us if you have any questions or you would like to get your own personalized Annuity Illustration.

With all of the different life insurance and retirement protection options available, it can be time consuming and overwhelming to figure out what to choose.

What I do is help you find the solutions that would

work best for you.

With all of the different retirement protection options available, it can be time consuming and overwhelming to figure out what to choose.

What I do is help you find the solutions that would

work best for you.

Contact Kirk Kanenbley

Calif. Life & Health License # 0M67527

Direct (909) 706-5737

Company (909) 498-4822

Office (909) 610-1810

Kirk's Social & Other Pages

Disclaimer: Disclaimer and Terms of Use

Professional Capacity

All information on this website is provided for educational and informational purposes only. Kirk Kanenbley is a licensed Life and Health Insurance Producer in the State of California (License #0M67527). The title "Retirement Planning Specialist" refers to his area of professional focus and expertise in insurance-based retirement products; he is not an investment advisor, attorney, or Certified Public Accountant (CPA).

Facebook

Instagram

X

LinkedIn